We all make mistakes, but we’ve also learned that some mistakes cost more than others do. This is especially true when you’re traveling. While no traveler can predict unexpected events like volcanic eruptions or earthquakes, there are a number of expensive mistakes travelers make often enough to warrant this post.

We all make mistakes, but we’ve also learned that some mistakes cost more than others do. This is especially true when you’re traveling. While no traveler can predict unexpected events like volcanic eruptions or earthquakes, there are a number of expensive mistakes travelers make often enough to warrant this post.

The following are some of the most expensive mistakes travelers common make – and how to avoid them.

1. Not checking your passport early

This mistake can happen to the best of us – after all, ten years is a long time and if you use your passport infrequently it’s easy to forget when it is due to expire.

Trip cancellation coverage with your travel insurance plan may cover your lost trip expenses if your passport is lost or stolen, but it won’t cover them if your passport has expired because that’s part of your good faith responsibility to verify.

In addition, entry into some countries like Costa Rica requires that your passport be valid for six months AFTER you arrive in the country. If you get turned away at the border for having an invalid passport, your travel insurance plan won’t reimburse you for your costs.

If you’re planning a trip where you’ll need your passport, check the expiration date early and for everyone who’s going on the trip. See the State Department’s information on how to get your passport in a hurry if you need to expedite your passport renewal..

2. Using your phone overseas

These days, our phones do far more than ever before – and many of us are ridiculously dependent on those services to find our way around, find a restaurant, keep everyone updated on our day, etc. But using your phone in a foreign country without an international plan can be shockingly expensive.

Of course, you could leave your phone behind and see what travel was like in the ‘old days’. If that’s too scary, you have lots of options to choose from to stay in touch without losing your shirt, including:

-

Get a temporary overseas plan with your provider for the duration of your trip.

-

Switch to a Voice over IP app like Skype to make calls when you find a Wi-Fi hotspot or use your 3G network.

-

Switch your phone’s SIM card, which you can buy locally and pay local rates.

-

Buy or rent a temporary pre-paid phone that works where you’re traveling.

-

Use a free hotspot and spend your time on social media (just remember to disable any automatic downloads).

See Does travel insurance cover phones to understand how to protect your phone.

3. Packing too much stuff

Nearly all of us struggle with this one and more than half of us return home with an outfit that was never worn on the trip. With baggage fees climbing steadily, it’s wise to rethink how much stuff you’re bringing with you and remember that you can buy something you’re missing on your trip.

Regularly check the weather reports for your destination – both current and historical data – to be sure the items you have are really what you need.

See these tips to lighten your load:

Avoid an expensive situation at check-in by reviewing your airlines’ baggage rules and weighing your bag ahead of time. An overweight bag can really bite into your available travel money.

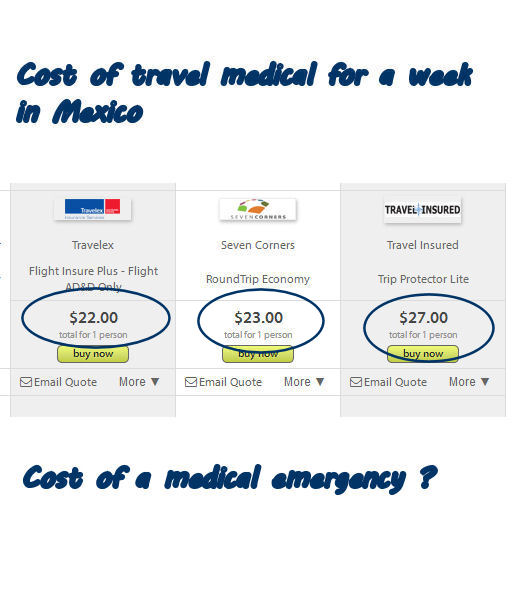

4. Traveling without medical insurance

Not one of us likes to spend money where it’s not necessary, but having travel medical insurance is not one of those scenarios. Sure, you might get through your entire trip without breaking your ankle on a cobblestone street, or contracting a severe case of norovirus, or slipping on the wet tiles at a spa, but if you do wind up in a hospital that’s outside your health insurance network, it can be an expensive financial blow.

Many countries require up-front payment for medical care even with travel insurance, and some travel insurance providers will pay the medical facility directly. If your travel insurance company reimburses you instead, you may need plenty of credit on your credit card.

Before you leave, contact your health insurance provider and find out what coverage you will have where you’re traveling. If there’s little or none, a travel medical plan is a cheap way to protect yourself.

5. Forgetting to tell your bank

If it’s unusual for your credit or debit card to have a charge for restaurant meal in Paris, then your bank may suspend your card for potential fraud. This is an excellent service when the charge isn’t your own and your card has been stolen, but it can be a real problem when you need to pay for your next purchase and the card has been cancelled.

Avoid this situation altogether by contacting your bank and let them know the dates and where you’ll be traveling. Be sure to give them both pieces of information and tell them how to get a hold of you on your trip – if you’re in Paris and a charge shows up on your account from Singapore, the bank will do what it’s trained to do and close your account anyway.

6. Making booking mistakes

Many of us are guilty of this one and it includes a wide range of mistakes:

-

Not leaving enough time between connecting flights

-

Not verifying our calendars and taking into account the time differences

-

Booking the wrong outbound or return flight

-

Booking a flight out of the wrong airport

Rebooking departure dates is one of the most common traveler mistakes and it happens all the time. You can make a lot of changes to airline tickets, but these days those changes can lead to a hefty fee. Double and triple check your calendar before making reservations.

7. Not reserving a place to stay – at least for the first night

Even the most spontaneous travelers need somewhere to put their suitcase – and perhaps their bum – down for the first night. Traveling can be hard on the human body and landing in an unfamiliar city without a reservation could prove more expensive than you think. Wandering around with heavy bags looking for a place to rest isn’t ideal either.

No matter how flexible you want your trip to be – have a place to stay the first night. Keep that reservation and hotel information handy so you can get directions from a local or give it to a cab driver.

8. Failing to research local transportation

What do you know about the transportation at your destination? If you’re staying in a friendly seaside village, do you know how you will get from the airport to that final destination? You can’t assume that the transportation system where you are traveling is similar to the one you have back home. You might be used to lots of cabs and buses being available at all times of the day and night, but try that in some regions of the world – especially if your plane was significantly delayed and you’re arriving late in the night – and you could end up sleeping in a park until morning.

Do a little research on the transportation so you know how far you’ll be going and how you’ll get there. If you’re planning to take public transportation, be sure you know what options you’ll have when you arrive. Also, it may be more cost-effective to buy your rail passes before you leave.

9. Taking the ‘typical tourist’ route

Staying on the standard tourist route is often the most expensive way to travel. While there are certainly some sites that are not to be missed on certain trips – the Eiffel Tower in Paris, for example – the simple demand for those views means they cost more. Visiting the less known destinations can significantly reduce the cost of your trip and often those are some of the most interesting places to visit.

The same is true for traveling during the high season. A destination’s peak travel period results in the highest demand and thus the highest prices. If you’re planning to travel during a busy time, book well in advance for the best prices. If you can travel during the off-season, however, you’ll save a lot of money but you may not have ideal weather conditions. The shoulder seasons are often ideal to get the best of both worlds.

Insurance")