On Sunday March 8th the US Department of State issues a statement advising US citizens to avoid travel on cruise ships, in response to the growing concerns of Coronavirus. The statement includes recommendations and we discuss on the show some of the key points.

Episode 1: How travel insurance covers Coronavirus

In this episode we talk quickly about how travel insurance covers cancellations due to Coronavirus, and tips on how to get coverage as we go forward.

Travel Insurance Coronavirus- How is the COVID-19 virus covered?

What you will find on this page:

Overview of Travel Insurance coverage for the Coronavirus outbreak

Travel insurance covers Coronavirus for medical emergencies, medical evacuations, interruptions, and cancellations if you are currently insured and meet the right conditions.

If you are currently insured and want to cancel because you are concerned about getting sick, that is not a typical covered reason for cancellation and you would not be covered. The only way you would be covered is if you have Cancel For Any Reason (CFAR) coverage.

If you are not currently insured and want to buy travel insurance to cover cancelling for Coronavirus, a regular plan would not cover it. It is no longer an unexpected and unforeseen event, and concern of getting sick is not a covered reason for cancellation.

If you are not currently insured, want to buy insurance, and want it to cover Coronavirus cancellation, the only option is a Cancel For Any Reason policy (see How to buy travel insurance for coronavirus below).

How is Coronavirus covered?

Travel insurance coverage for Coronavirus can touch on several areas, which I will outline below.

If you currently have travel insurance

If you already have travel insurance, you might have coverage for the following situations:

Trip Cancellation– Travel insurance covers cancellations if you, a traveling companion, or a family member becomes ill and cannot travel. A physician needs to verify that you are unable to travel, but this is a common reason for cancellation.

Trip Interruption– Travel insurance also covers interrupted trips if it needs to be cut short. You can be reimbursed for lost expenses if you, a traveling companion, or a family member becomes ill and you need to cancel the trip partway through.

Medical Emergencies– Travel insurance covers emergency medical expenses for the insured if you get sick while on your trip.

Emergency Evacuation– If you become seriously ill on your trip and need to be transported home, it is covered by travel insurance.

If you do not currently have travel insurance

If you are planning a trip and want to buy trip insurance, you would have the following coverage regarding Coronavirus:

Trip Cancellation– You would have coverage in the general covered reasons for cancellation, if some got sick from Coronavirus. But, cancelling out of fear of getting Coronavirus would not be covered.

Trip Interruption– You would have coverage in general for interrupted trips if it needs to be cut short. You can be reimbursed for lost expenses if you, a traveling companion, or a family member becomes ill and you need to cancel the trip partway through.

Medical Emergencies– Travel insurance would covers emergency medical expenses for the insured if you get Coronavirus on your trip.

Emergency Evacuation– If you become seriously ill from Coronavirus on your trip and need to be transported home, it is covered by travel insurance. This is generally very rare.

Summary of coverage for Coronavirus

There are many combinations of how this is all covered, so I’ll summarize below:

- Travel insurance covers Coronavirus like any other illness. Any coverage related to an illness such as cancellation, interruption, medical , and evacuation would have the same coverage for Coronavirus.

- Travel insurance does not cover cancelling a trip because you are concerned about getting sick. This is not a covered reason for trip cancellation.

- The only option for cancel out of concern for getting sick is with Cancel For Any Reason coverage.

Cancel For Any Reason travel insurance

The best travel insurance option is you want “peace of mind” for whatever happens is Cancel For Any Reason coverage.

Cancel For Any Reason is a policy upgrade that lets you cancel your trip at your choosing, for any reason. This extends the standard covered reasons for trip cancellation.

Requirements for this coverage:

- You need to insure 100% of your trip costs

- You need to buy it soon after your first trip payment, usually 10-30 days

- You need to cancel your trip at least 48 hours before departure

*Also note, CFAR does not reimburse 100% of your trip cost, but usually up to 75% of the insured trip cost.

How does Cancel For Any Reason coverage work?

Cancel For Any Reason is an upgrade to a typical plan. It costs more because it covers a lot more, and the insurance company has higher risk of paying a claim.

You can get CFAR coverage 2 ways:

- Many plans allow you to “upgrade” to CFAR coverage for a fee

- Some plans automatically include CFAR and are priced accordingly

How to buy travel insurance for Coronavirus

As stated above, when it comes to buying travel insurance for Coronavirus-related issues, there are two options:

Option 1- Get standard travel insurance and you are covered with Coronavirus like with any other illness. This costs less but you cannot cancel because you are afraid of traveling.

Option 2- Get Cancel For Any Reason (CFAR) coverage, and you have both the standard covered reasons for cancellation (which pay 100% of your expenses), but can also cancel for any reason and get most of your expenses reimbursed (up to 75%).

For a complete tutorial, read our How to Compare Travel Insurance tutorial.

Here is a short version for comparing plans for Coronavirus coverage.

Time needed:Â 15 minutes.

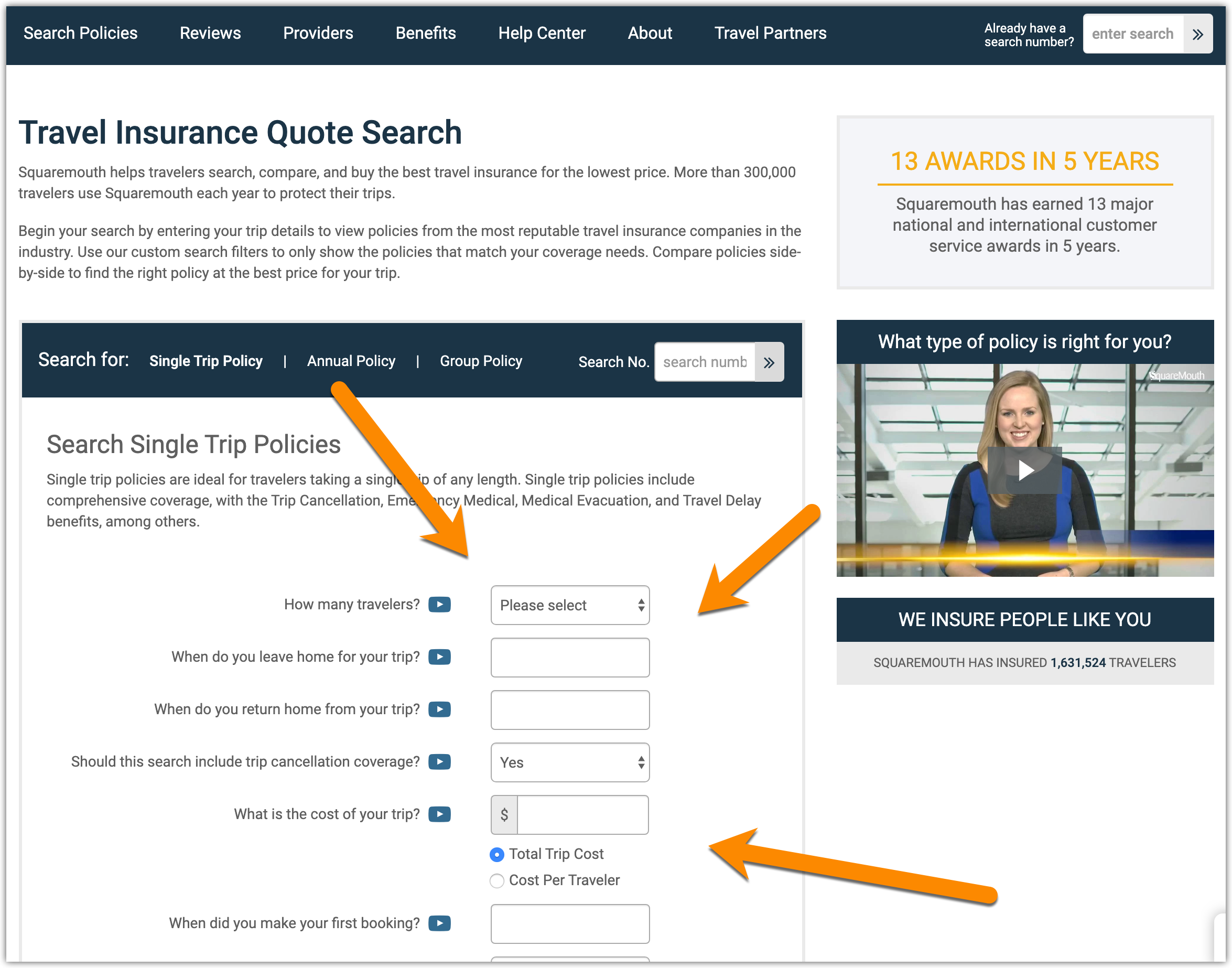

How to quote, compare, and purchase travel insurance:

- Use a comparison engine to get quotes from all companies

You can get quotes from all major companies through our partner website Squaremouth.com.

- Enter your trip details

Here you will enter information about your trip like traveler ages, travel dates, cost, deposit date, destination, and residency.

- Click “Search Now” when finished

After entering your trip information, click the Search Now button.

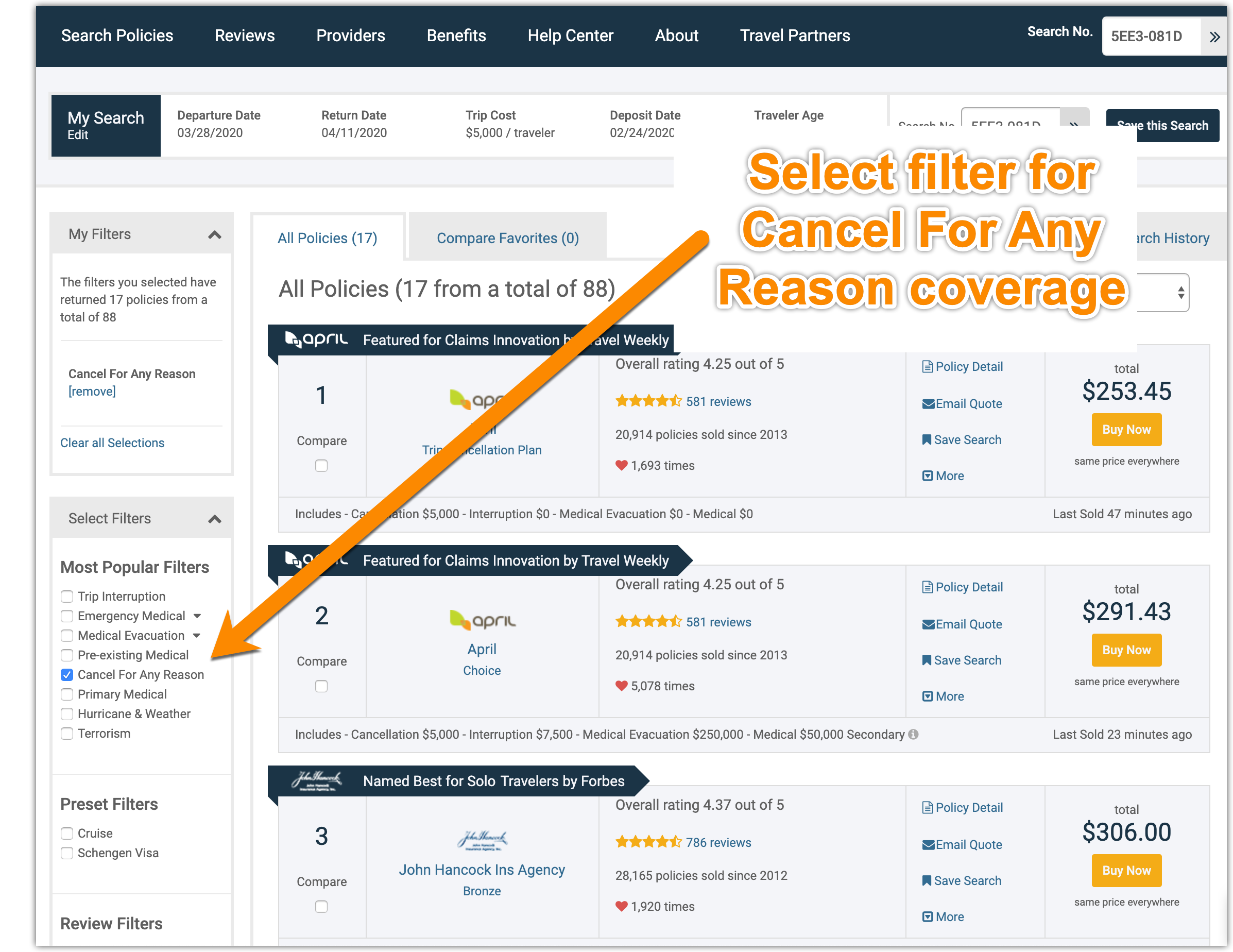

- View results screen

Next you will be shown quotes from all major companies and policies.

- Check filter for “Cancel For Any Reason” coverage to see plans with that option

To see plans with the CFAR coverage, check the filter box on the left side of the results screen. This will show only plans with this coverage, and let you see the price difference between plans with and without CFAR coverage.

- Choose a plan and click “Buy Now” to purchase

To help you find the best plan, you can apply other filters for different coverage amounts. You can also select several plans and compare them side-by-side, which helps see how the coverage compares easily.

- You will receive an immediate email confirmation of coverage

When you are done, you will receive an immediate email with a confirmation of coverage and printable documents to take with you on your trip.

Frequently Asked Questions

I want to cancel my travel plans because I’m afraid to travel due to the Coronavirus, is that covered?

No, trip cancellation for concern or fear of travel associated with sickness, epidemic, or pandemic is not covered under travel insurance covered reasons.

Are cancelled flights covered for Coronavirus?

If an airline cancels a flight, they should reimburse you for the cost of the flight. This would not be covered by travel insurance.

Am I covered if I get Coronavirus?

Emergency medical coverage (part of travel insurance) would cover any medical expenses from coronavirus if you get sick during your coverage period.

Is being quarantined for Coronavirus covered?

If you are quarantined you can have coverage under the Trip Interruption benefit of your policy.

If I get coronavirus on a cruise ship, will travel insurance help evacuate me?

It is very uncommon for travel insurance companies to arrange for evacuation off of a cruise ship. Typically, you have to be hospitalized first and the assistance company will work with the attending physician to arrange transportation to another hospital, or back home if required. This would mean heading to a port-of-call.

Links for Coronavirus Resources

Outside the topic of travel insurance for Coronavirus, here are some great resources.

Ryanair and easyJet fined for mis-leading travel insurance sales

Two European airlines have been fined for their mis-leading practices in the sales of travel insurance.

Ryanair and easyJet, of Ireland and England respectively, have been fined a total of 1,000,000 Euro by an Italian regulator. They claim that both airlines had unfair practices in the sales of travel insurance, including ‘opt-out’ sales and not providing information about the policies being sold.

“Opt in” travel insurance should be used cautiously

We have written about opt-in travel insurance before, which is an up-selling technique that many booking sites use. As you work through your purchase, you are presented with a very simple way to click a box and buy insurance. The plan is usually a low flat rate, and the total effort is clicking a box and the premium is added to your total.

This is obviously a very easy (and profitable) way to sell travel insurance because there is little effort required. It shows a low price, a check box, and a headline such as “Protect Your Trip With Insurance”. But most travelers who buy this way are not actually reading their policy and understanding what they are buying. The coverage is assumed, and if they need to file a claim there is often a misunderstanding about what is covered.

The other practice we have written about is ‘opt-out’ travel insurance, which is even more dangerous.

In this case, the check box is already selected, and if you don’t uncheck it (opt out) you are buying the plan. The Department of Transportation has made this illegal since 2012, and rightly so.

The best way is to buy separately from a 3rd party

I recommend researching and buying travel insurance from a 3rd party.

This separates the purchase and allows you time to fully understand what you are buying. You will have a better selection of plans, and often get better pricing due to this competitive selection.

Sometimes what you are buying is not actually travel insurance, but another concept called ‘travel protection’. This type of purchase is totally different from insurance, and should be avoided as well.

Hostel Travel: 4 Tips to Insure this Trip

Did you know there are hostels to fit every type of travel? We were surprised too, but we found that some hostel sites define different types of hostels – luxury, romantic, family, etc.  –  and tag them by activity  – ski, party, beach. You can even find designations for the structure in which the hostel is lodged: prisons, haunted houses, ryokans, and more.

Did you know there are hostels to fit every type of travel? We were surprised too, but we found that some hostel sites define different types of hostels – luxury, romantic, family, etc.  –  and tag them by activity  – ski, party, beach. You can even find designations for the structure in which the hostel is lodged: prisons, haunted houses, ryokans, and more.

Many people believe that hostel travel is only done by the young, single backpacker on a budget, but these days there are hostels to fit nearly every type of traveler. Most hostel travelers are watching their budgets, but they also enjoy the experience of staying in a hostel for a range of reasons. Some hostels give you a lively social scene, for example, and the opportunity to make friends. Not all hostels are like big, open dorm rooms either – many have separate rooms for 1, 2, 3, or more travelers who want a little more privacy.

Of course any trip comes with risks and limiting your exposure to travel risks is what travel insurance is all about. We looked into what hostel travelers should know about insuring their hostel trips and came up with the following tips.

1. No traveler expects to have to cancel

It’s important to understand the range of reasons that could cause you to cancel your trip and some may surprise you:

-

You’re in a traffic accident just days before your trip and not recovered enough to travel

-

A family member is diagnosed with cancer, and you want to help with their care (you can travel once the cancer is gone)

-

You’re unexpectedly offered the job-of-a-lifetime, but you have to start tomorrow

-

Your best friend commits suicide and you just can’t stand the thought of leaving right now

Most of the time the reason a traveler has to cancel any trip is completely unexpected. It’s a surprise entirely out of the blue; something you’d never predict happening. Of course, that’s the intent behind insurance. After all, no homeowner expects to see their house burn down in a wildfire, but these things happen.

If you are taking a trip and you’ve spent money on that trip that you cannot afford – or would prefer not – to lose, then insuring that trip against cancellation is a wise idea. When you insure a trip for cancellation, you are insuring the pre-paid costs that are non-refundable. Anything you pay for before you leave – hostel reservations, airline tickets, train tickets, etc. – is a pre-paid trip expense. Some of those expenses are refundable in certain circumstances, but many are not. After all, they want their money too and cancellation policies are written to protect the one who has your cash.

2. Getting home fast can be difficult and expensive

Just like covering your trip for cancellations, it’s important to have a plan for how to get home should you be called home in a hurry. No one expects that their little sister will be in a tragic accident on her way to school, after all, but if you’re traveling wouldn’t you cancel your trip and head home to be with her and your family if they needed you?

Last-minute flights are expensive, especially if you already paid for your return trip ticket. The airlines are a lot less forgiving than they used to be about flight changes – even for emergencies. In some cases, the cost of changing a flight can be worth the price of a new ticket.

Travel insurance plans include trip interruption coverage, which is designed to get a traveler home in a hurry, and 24/7 traveler support for emergencies.

Trip interruption coverage reimburses the traveler for unexpected, and often expensive, travel costs like last-minute airfare, lodging, taxis and more. It can even reimburse a traveler for the portion of their trip they didn’t get to use because of the interruption – so you can travel again once the emergency is handled.

Travel assistance services can help a traveler arrange last-minute travel home.

3. Emergency medical care is always expensive

The cost of medical care is expensive no matter where you travel and when you travel outside your home country, your health insurance plan (if you have one) doesn’t usually cover your medical costs overseas.

Young people – especially active young people – have medical emergencies and if you’re traveling in a foreign country you may be required to pay for your medical care up-front. Unless you’re willing to put your credit card on the line to pay for x-rays, surgery, bandages, medicines, a doctor’s time, and more, you should have travel medical coverage.

Luckily, travel medical coverage is very affordable and even more so for young travelers. It’s almost a no-brainer when it comes to traveling outside the country where a foreign government is simply not responsible for taking care of your medical needs.

4. Baggage gets pilfered

No one is completely safe from thieves no matter where you go, but travelers can minimize their exposure to risk by leaving the valuables at home, carrying limited amounts of cash, using a money belt, and more.

Many hostels also provide lockers that travelers can use to protect their belongings and hostel travelers know to bring their own locks. A little research in advance will let you know if you will have lockers available.

Coverage for lost, stolen, or delayed bags with a travel insurance plan can help the hostel traveler in several ways:

-

If your bag is temporarily delayed, you can get a fresh change of clothes and some basic personal items to get you through until your bag arrives.

-

If your bag is irretrievably lost or stolen, you can be reimbursed for the clothing, personal items, etc. you have to buy to get through your trip (including a bag to take it all home).

There are a number of limits to baggage coverage, including a minimum number of hours before the delay coverage kicks in, and more. Click the links above for a better understanding of baggage coverage with your travel insurance plan.

What’s the Cost to Insure this Hostel Trip?

Let’s take a look at a hostel trip and what you might need to insure on this trip.

Let’s say a group of four college friends will be traveling for two weeks in Amsterdam. They are coming from all over the country and haven’t seen each other since graduation.

-

Tom – Los Angeles is spending $1,149 for airfare

-

Steve – Seattle is spending $1,166 for airfare

-

Owen – Newport is spending $992 for airfare

-

Matt – Dallas is spending $936 in airfare

They settled on staying at a downtown hostel because it’s in a great walkable location with lots of nightlife, museums, and cafes nearby – ideal for younger travelers who don’t want to rent a car.

To save money, they chose to reserve their rooms as non-refundable. They reserved a 4 bed suite to share at just $245 or $61.25 each. Each traveler will want to insure their pre-paid trip costs – their airfare + their portion of the hostel cost.

Each traveler also has individual concerns for this trip:

-

Avid cyclists, Tom and Matt are taking along their road bikes and plan to ride each day.

-

Steve and Own are self-employed and each is taking a laptop to keep tabs on work.

Tom and Matt will want a plan that includes baggage coverage for their bicycles in case they are stolen or lost along the trip. Baggage coverage with most travel insurance plans includes coverage for bicycles, but the total coverage for any one stolen item is not high. So they may want to choose a plan with a higher limit for baggage coverage. Riding your bike on streets is not considered a hazardous sport by the travel insurance companies, and so they don’t need adventure coverage.

Owen and Matt should understand that there is limited coverage for electronics with any travel insurance plan. They can talk with their homeowner’s policy and cover the electronics that way, but otherwise they should plan to carry them onto the plane and keep them locked in the hostel safe or in private lockers when not in use.

See our techniques for keeping valuable safe while traveling for more ideas.

Here are Tom’s trip details plugged into our travel insurance comparison tool:

Tom chooses plans with a little higher per-item limit (at least $1,000) on the baggage coverage for his bike:

This image shows just a couple of plans to give you an idea of the cost, which you can see is very affordable for benefits like 100% trip cancellation, 150% trip interruption, $25,000 – $50,000 in emergency medical (in case he falls on a ride), and more.

8 Steps to Verify You Have the Right Travel Insurance

One of the biggest complaints travelers have about travel insurance is that it doesn’t pay out when they expect it to. In nearly all of the cases we’ve seen over the years it comes down to the traveler not understanding what their plan covers and, more importantly, what it doesn’t.

One of the biggest complaints travelers have about travel insurance is that it doesn’t pay out when they expect it to. In nearly all of the cases we’ve seen over the years it comes down to the traveler not understanding what their plan covers and, more importantly, what it doesn’t.

Travelers buy travel insurance for all kinds of reasons:

-

‘I’m worried about terrorist attacks and want to be protected.’

-

‘My parents are elderly and I want to be able to get home if they need my help.’

-

‘If I get hurt or sick, I don’t want to worry about paying a huge medical bill.’

-

‘My job has been a little ‘weird’ lately and I’m worried about layoffs.’

To be sure you actually have the right travel insurance for your trip, follow these steps with the plan you already purchased or want to purchase. Check your plan within the review period so you still have time to cancel your policy (for a refund) or make changes to get the coverage you need.

1. Do a quick health review

If you’ve been to the doctor recently – is that condition likely to recur? If you visited the doctor for migraine headaches in the past few months, for example, and that condition reoccurs on your trip, your medical care while traveling might not be covered.

Why?

Because the condition is considered pre-existing and most travel insurance plans exclude medical care for pre-existing conditions. A traveler who has a pre-existing condition can purchase a plan with coverage if they purchase it soon after their first trip payment or buy the optional upgrade. Some travel insurance plans cover pre-existing conditions automatically if the plan is purchased early. No travel insurance plans cover losses due to mental health issues or suicide.

Very Important: be warned that the exclusions for pre-existing medical conditions apply not only to the traveler but also to family members and travel companions. Most people don’t have the full details of another’s health history, but if a close relative or business associate’s state of health leads to a decision to cancel your travel plans, that cancellation may not be covered if the cancellation was due to a pre-existing medical condition.

2. Check your destination

To get the latest health and security information about where you’re going, you have a number of sources outside of the standard media coverage.

-

To find out the latest travel safety information – including warnings about the potential for terrorist actions, see the State Department Website.

-

To find the latest health information – including information about recommended vaccines the latest outbreaks, see the Traveler’s Health section of the CDC Website.

Check out our topic on the Best Places for Travel Health and Safety Info for more details.

3. Check your travel mileage

How far you travel factors into a number of travel insurance benefits. Most travel insurance policies limit the coverage unless a traveler is going a certain distance from home. For example:

-

If you’re traveling abroad, you are likely to be outside your health insurance network on your trip. That means you won’t have benefits for emergency medical treatment without travel medical coverage.

-

If you’re traveling within your home country, the benefits for medical evacuations and repatriation may not be in effect.

The key is to be sure your destination is far enough to warrant the coverage you’re paying for.

4. Know your trip activities

The activities you do on your trip could render your coverage invalid. Travel insurance plans typically exclude a number of activities that are considered more hazardous than say running along the beach in the dark. Specifically activities like parasailing, hang-gliding, mountain sports, diving and more are excluded from the typical plan unless you purchase an upgrade.

Some travel insurance plans are designed specifically for adventure travelers, but even if you’re a typical traveler and don’t plan on doing anything potentially dangerous, you could run into a unique opportunity to do something adventurous on your trip.

Take out your travel insurance policy documentation and read the section labeled ‘Exclusions’ to know which activities could cause your policy to be useless. You don’t want to find out that rock climbing is a non-covered activity after you fall and get hurt. Know ahead of time.

5. Double check the dates

In the chaos of planning a trip, the dates may get shuffled around a little so you can get the best airfare or meet a friend while waiting for a connecting flight. The key is to double check that the dates you are traveling are the dates you’re covered for with your travel insurance plan. Everything has to match up correctly if you later have to make a travel insurance claim.

The same is true for the traveler’s ages, names, etc. Scrutinize the details and call your travel insurance provider as soon as you identify a discrepancy so the change can be made ahead of time. Once you depart, these changes can’t be made.

6. Verify your layovers

Travel insurance coverage for trip delays and missed connections comes with the standard caveat that you gave yourself enough time from the start. If you schedule a multi-stop flight with tight connections and the first flight is delayed for an hour due to mechanical repairs, you could throw off your entire trip.

Even worse, if the delay means you incur a loss and want to make a claim on your travel insurance plan they will verify that you had enough time to make your connection.

7. Check the policy limits

Every insurance plan has limits applied to the coverage. The baggage limits, for example, may not be enough to fully reimburse you for a lost bag and it’s contents (depending on what you’re taking with you). Where the limits really get sticky are when it comes to medical and evacuation coverage. Specifically, you want to have enough coverage to pay for these events should they occur, but you don’t want to pay too much for coverage you may never use.

It’s a tricky balance, but luckily our travel insurance comparison tool offers some suggestions based on your age, your destination, etc. to help you determine how much travel medical and evacuation is enough.

8. Don’t make assumptions

Don’t make assumptions about your travel insurance coverage. Many travelers read that their policy covers trip cancellation, for example, and assume it means the plan will cover no matter what causes the cancellation. Or, they read that their plan covers travel delays but they don’t understand that the delay must meet a minimum number of hours.

If you have a specific concern, read your travel insurance policy (or the description of coverage) before you buy or or soon after so you understand your concerns are covered.

If you’re worried about the possibility of losing your job, for example, and you want to be sure you can cancel your trip and be reimbursed your non-refundable trip costs, make sure that job loss is listed as a covered reason and that your length of employment meets the requirements (usually at least a year is required).

Getting the right travel insurance takes a little bit of thinking, some research, and a careful review of the policy you choose. It’s not hard, but it does take a little effort on your part. See the 9 Most Expensive Travel Mistakes You’re Likely to Make for more details on what to watch out for.

8 Ways Travel Insurance Protects You from Terrorists

The terror attacks of September 11, 2001 were like nothing the traveling public had ever seen before. When a terrorist attack occurs, travelers understandably get nervous and wonder whether they should cancel their travel plans.

The terror attacks of September 11, 2001 were like nothing the traveling public had ever seen before. When a terrorist attack occurs, travelers understandably get nervous and wonder whether they should cancel their travel plans.

Some travel insurance plans exclusively prohibit any claims due to terrorist attacks and others list incidents of terrorism as a covered reason for travelers to make a claim on their various travel insurance benefits. The key is that a terrorist incident must be listed in the policy as a covered reason for canceling your trip, going home early, accessing medical care, etc.

There are, of course, limits to the coverage for terrorist incidents with a travel insurance plan. It’s important to note that most travel insurance plans state that the terrorist incident must have occurred recently (usually within 30 days of your departure) and it must be in or within a certain number of miles from a city listed on your itinerary.

The following are 8 ways travel insurance protects travelers from terrorists.

1. Cancel your trip and get your money back

Many travel insurance plans allow the insured traveler to cancel their trip prior to leaving when a terrorist attack occurs. This is a great way to protect your trip investment from the actions of terrorists.

If your destination is a long way from where the terrorist act occurred, but you want to cancel your trip for fear of follow-on attacks, you’ll need to have ‘cancel for any reason’ coverage to make a claim.

2. Go home when terrorists strike

If a terrorist incident occurs where you are traveling and you want to leave the area and go home, trip interruption coverage will reimburse the insured traveler for additional transportation expenses (up to the plan limit) less any money you receive from the exchange of your airline ticket (if any).

Depending on how much of your trip remains, you may also be reimbursed for the non-refundable trip costs you paid for but didn’t use prior to heading home.

3. Get medical treatment when injured in a terrorist attack

While travel insurance providers place limits on some coverage for terrorist attacks, there is no such limitation on medical treatment when the traveler is injured in a terrorist attack. If you are in a foreign country and caught in a terrorist attack, your emergency medical treatment will be covered up to the limits of the travel insurance plan.

Acts of terrorism and terrorist incidents must not be listed under the general exclusions for this benefit to be available to a traveler caught in a terrorist incident.

4. Send your kids to college even if you’re dead

Most travel insurance plans include some Accidental Death and Dismemberment (AD&D) or flight accident coverage. If you are killed during a terrorist incident while on an insured trip, your beneficiaries will receive the amount of money listed in the policy details. This benefit if secondary to any other life insurance or AD&D you have through your employer or other sources.

5. Catch a ride out the mess

When a terrorist does their worst, the insured travelers are in a much better position to catch a ride out of the area where the terrorist action has occurred. Many travel insurance providers offer security or political evacuation coverage and they will retrieve their covered travelers and take them to a safer place.

6. Manage delays caused by terrorism

Many travel insurance plans list travel delays as one of the covered events. If you are delayed from reaching your destination due to a terrorist act, you’ll have the money you need to cover unexpected lodging and transportation among other things. You’ll also have the support of the travel assistance services to book hotel rooms, re-arrange flights, and much more.

7. Recover your body

If you are killed in a terrorist incident while traveling, a travel insurance plan with coverage for the return of mortal remains, or repatriation, will work to recover your body and return it home for burial. The travel assistance team will negotiate with government officials, handle the paperwork, arrange and pay for the shipping costs to ensure that your body is safely returned home.

8. Help if you’re hospitalized

If you are traveling with your children and you are hospitalized as a result of a terrorist attack, many travel insurance plans include coverage to return minor children to their home or to a suitable caregiver while you recover. Another little-known benefit of travel insurance is one called bedside visit or emergency medical reunion. This benefit brings a family member or friend to your bedside if you will be hospitalized in a foreign country for a minimum number of days (usually 7).

Your Definition of Terrorism May Not Match Theirs

When a travel alert or warning is issued by the U.S. Department of State and warns travelers about the potential for terrorist acts in the near future, many travelers scramble to find their travel insurance plans and review their coverage. As they say, “the devil is in the details.†What you might identify as a terrorist incident may not be identified as such by others – specifically by your travel insurance provider.

The terminology of the travel insurance plan plays an important part. If the event does not turn out to be caused by a terrorist as defined by the terms of the policy, your claim will be denied.

Let’s look at how some plans define terrorist incidents. The following one is from Travel Guard’s Platinum travel plan:

Another travel insurance company – Travel Insured International – defines terrorist incidents as follows:

In the second case, the terrorist act must be identified as such from the U.S. government. If a train blows up in the city where you are visiting and you think it’s a terrorist action and make a claim for trip interruption when you return home, your claim will only be paid when (and if) the U.S. government identifies it as an act of terrorism. Otherwise, your claim will be held in limbo until the matter is decided by the government.

While insured travelers have some protection against terrorist acts (depending on the plan they chose), there is no coverage for terrorist threats – even when the warning is issued by the U.S. government. Your only guarantee that you will be able to cancel your trip and recover some or all of your trip investment is to have ‘cancel for any reason’ coverage with your travel insurance plan.

6 Tips for Insuring Green Travel

The term green travel conjures many different images for travelers – sleeping in a hammock slung between two trees at a public beach, for example. For most travelers, however there are various shades of green travel that involve a range of actions that are far easier to implement.

The term green travel conjures many different images for travelers – sleeping in a hammock slung between two trees at a public beach, for example. For most travelers, however there are various shades of green travel that involve a range of actions that are far easier to implement.

At the heart of the matter is the universal view of the importance of protecting the natural and cultural environments of places you’re visiting. That means implementing habits that preserve the plants, wildlife, and other resources in their most natural state and respecting the local culture while contributing positively to local communities.

Many travelers believe that taking a green approach to travel makes for a more rewarding and authentic travel experience. It encourages travelers to create deeper connections with the people they meet and the places they visit.

Just like back home, you can take going green about as far as you’re comfortable. Many travelers implement simple ways to green-up their travel:

-

Choosing green lodging – these are hotels that employ locals, have recycling and linen reuse programs, and give back to the local community. Some green lodging really is renting a hammock on the beach, but other options including working on local farms, Â renting local apartments, or exchanging homes.

-

Taking public transportation, walking, or biking – these are all great options for reducing the amount of carbon emissions a traveler causes when they travel. Many cities have begun implementing bike exchanges, for example, and you can often find some of the best tours of cities by hiring a walking tour guide to give you the local, grounds-eye view of a new destination.

-

Carrying a refillable water bottle – if you’re flying, you’ll need to empty it before you go through security, but you can refill it on the other side and you won’t be buying and tossing water bottles as you travel. You can even get water bottles that filter the water for impurities now so the water you’re drinking is a little safer.

-

Avoiding takeout in non-recyclable containers – as a traveler, you may not be in the position to cook where you’re staying, so buying your food as you go is part of the travel experience. Street vendor foods and even restaurant leftovers can often be wrapped in just a little paper or recyclable aluminium foil rather than in products that cannot be recycled and cause a greater landfill footprint (think styrofoam).

-

Booking non-stop flights – a significant portion of a plane’s carbon emissions comes from the takeoff and landing, so reducing the stops helps a traveler’s overall carbon footprint.

-

Buying local when you arrive – this means choosing local restaurants that buy their products from local farmers instead of hitting the chain that imports everything. Some travelers skip the TSA hassle and buy their shampoo, sunscreen, lotion and other liquids when they arrive. This helps the local economy and makes for an easier trip through security. Donate what’s left to a local shelter or drop it off at a hostel and it will get used up.

Taking a green approach to travel has become important for many travelers and travel suppliers such as hotels and tour operators have heard the call and made options available to travelers who want to go green, but what does a green traveler have to think about when it comes to insuring their trip?

1. Missed connections extend beyond the airlines

A missed connection occurs when a traveler fails to meet a scheduled departure due to severe weather, road closures, labor strikes, or simple errors. Missed connections aren’t isolated to problems with flights. Public transportation can be shut down, roads may be closed, severe weather may stop all ferries from carrying passengers and cars.

When a traveler misses an important connection, they may be forced to purchase new tickets to catch up to their tour. They may have to purchase new lodging and wait for the next shuttle, ferry, or train to take them where they are going. They may be forced to hole up in a hotel and wait out a storm. Either way, it means unexpected and unplanned-for extra expenses and travel insurance with missed connection coverage can help.

2. Cancelling your green travel means losing money

Even green travelers have some pre-paid and usually non-refundable trip expenses. If you’ve taken advantage of an online deal for your green lodging, it often comes with a cancellation policy that means you’ll lose all your investment if you have to cancel. Non-stop flights are sometimes more expensive than those that take a stop or two to pick up more passengers and cancelling means losing that money as well.

When you’re traveling green, you may take advantage of early purchase or discounted travel arrangements and many of those come with strict cancellation rules. If your kid gets sick, or a parent dies, or your passport is stolen, you could be out a lot of money no matter what your style of travel is. Insuring your trip for potential cancellations is the only way to be sure you can get your money back and travel another time.

3. Getting evacuated from a remote village is expensive

For some travelers, green travel means going to very remote places and the more remote the better. If you get injured or find yourself severely ill in a remote location, local medical care may not be nearby and arranging an evacuation from a remote location is time-consuming, complicated, and expensive.

When you travel green and you take your travel to remote locations, it’s important to have emergency medical evacuation coverage from a travel insurance company. They’ll arrange and pay for the costs required to transport you to a medical facility where you can be treated. They’ll also bring you home once you’re stabilized.

4. Medical care may not be available or reliable

The State Department’s travel destination information indicates many locations in the world that are ideal for green travel but have little in the way of close, reliable medical care. If you’re thrown from a donkey while riding a trail in the mountains of Argentina, you may be able to be transported to a medical facility but the local doctors are going to want up-front payment before they treat you beyond basic life-saving measures.

If your health insurance back home doesn’t cover your medical bills where you’re traveling (and many don’t – even Medicare doesn’t extend beyond the U.S. borders) then you could be paying for your medical care by credit card. Buying a travel insurance plan with coverage for medical emergencies means you can be reimbursed for your costs and many travel insurance providers will pay the medical facility directly – a fact that could speed up your treatment.

5. Baggage thieves could leave you nothing to wear

No country is immune from theft and your bag – even when you carry it on the plane – passes through many hands when you travel. In some situations, green travelers are at a higher risk of baggage theft simply because of their exposure. Your baggage may be tossed on top of a bus or strapped to the back of a bike taxi, but it’s always at risk of being stolen or pilfered – especially when you’re distracted by the sights and sounds of your new destination.

A travel insurance plan with coverage for lost or stolen baggage means that you can will be reimbursed for items that are stolen from your baggage. Read our review of baggage coverage or more details.

6. Going green doesn’t have to mean going it alone

Just because you’ve committed to traveling green doesn’t mean you have to go it alone. When you’re in a foreign emergency room having your foot stitched up, it can be a great relief to have a multi-lingual travel insurance representative helping you with interpretations. If it turns out your green hotel overbooked their rooms and you have no place to get some rest, your travel insurance concierge services can help you find another hotel nearby.

Travel insurance plans come with worldwide travel assistance services and the representatives are available 24/7 to help their members who get stuck in sticky travel situations. All it takes is a phone call to get the help you need.

7 Travel Insurance Tips for Extended Business Trips

Many business travelers find that extending their business travel – at least at some locations – is an affordable way to pack a little fun and discovery into their business trips.

Many business travelers find that extending their business travel – at least at some locations – is an affordable way to pack a little fun and discovery into their business trips.

A three-day business convention in London, for example, can easily be turned into a week-long family vacation with four days for pleasure. By combining business with pleasure, business travelers can often take advantage of ‘free’ airfare paid for by their employer by simply pushing their return date out a few days and then picking up the costs for the pleasure portion of their trip on their own.

The trend is catching on too. Many conferences now offer on-site child care for those attendees who want to extend their business trip into a family vacation.

A business trip, like any other trip, needs to be carefully planned and the travel insurance aspect must be addressed. If your company has a travel department and encourages pleasure extensions, you’re way ahead of the game. If they further cover their employees with business travel insurance plans, you’ve got some support for the business portion of your trip but perhaps not the pleasure portion of your trip. If you have to plan your business travel yourself, you’re going to want to look into your travel insurance options to be sure the business AND pleasure components are covered.

Here’s what you need to think about before extending your next business trip:

1. Does your health coverage extend to this travel?

Some business travelers are covered by their health coverage while traveling for business – some are not and so this is an especially critical concern. Before you take any business trip that’s outside your health insurance network, it’s important to make sure that you have health coverage for where you’re traveling.

When you’ve extended your business trip for pleasure, that health coverage that applied to the business portion of your trip may not be available to you if you’re outside the standard health care network. If you get injured while hiking in New Zealand after a long week of business strategy meetings, will your health care cover those medical costs or not?

This is an especially grey area of health care coverage and it could require some research through your benefits department and even by calling the health insurance company representatives.

It’s important to realize that travel medical insurance is very affordable – one of the most affordable types of travel insurance and often worth the purchase simply for the peace of mind.

2. What if your business trip is cancelled?

If the business portion of your trip is suddenly cancelled, the company takes the hit on the pre-paid trip costs, but if your pleasure trip was combined with the business trip you may have some cancellation concerns of your own.

In some cases, your employer may simply let you repay the company for the airfare and you can take the extra time for pleasure, but that’s something you’ll have to work out with your employer.

Here’s how to avoid a big loss if the business portion of your trip is cancelled and you can’t go:

-

Schedule your lodging with places that allow last-minute cancellations. You may have to pay a higher per-night price, but it could be worth it.

-

Pay for tours and other trip costs when you arrive, and not before. Again, this might mean paying a slightly higher per-ticket price, but you won’t be out the entire amount if your trip is cancelled and you can’t go.

-

If family members were to travel with you on the business trip, consider covering their airfare with ‘cancel for any reason’ trip cancellation coverage. If your business trip is cancelled but your airfare was not included in the trip cancellation coverage, the standard covered reasons for cancelling likely will not apply and your claim will be denied.

Essentially, you want to be sure you limit your out-of-pocket non-refundable trip costs just in case the business trip is cancelled.

3. How is your baggage covered?

When you travel for business, what goes in your bag is very different from when you travel for pleasure. Business suits replace bathing suits, laptops and display equipment replace your e-reader, and you could be hauling quite a bit of promotional material. Many business travelers have corporate credit cards with extended travel benefits – often covering items like luggage. Now is a good time to call the credit card company and have them send you the latest copy of your travel benefits – ask for the fine print version.

Read that carefully to determine if you:

-

Have coverage for all the items you’re taking for your business trip. If the equipment you’re taking along is worth more than you’re covered for, consider insuring it another way or shipping it ahead of time with extended insurance applied.

-

Have coverage for your personal items while on the extended portion of your trip. Sometimes the travel benefits are very specific and they won’t cover personal items that aren’t related to your business travel.

If you don’t have coverage for the stuff you’re taking along, check with your employer benefits department to see if your business travel coverage includes it. If not there either, it might be time to apply some travel insurance to your trip simply to be sure your business and personal items arrive intact and if they don’t, you’ll have some coverage to get them replaced in time to take care of business. See our full review of baggage coverage for details and review the baggage delay coverage information too.

4. Do you have a system for receipts?

Long gone are the days of the free-spending business traveler with a fat business account and little spending oversight. The receipts that apply to the business portion of your trip – hotel stays, meals, transportation are usually paid for your company but you’ll want to keep those carefully separate from those that apply to the pleasure portion of your trip.

5. Are you covered for travel delay costs?

Travel delays occur for all kinds of reasons – volcanic eruptions, terrorist attacks, severe weather, and more. When your travel is delayed and you incur additional unexpected expenses for lodging, meals, transportation, and other fees, do you have to pay for those yourself or does the company pick up the tab. If you’re on the pleasure part of your extended business trip, those costs may be yours to cover and a travel insurance plan with travel delay coverage can make a big difference.

6. Are you covered for evacuations?

A business traveler doesn’t always have the luxury of traveling to safe locations and yet, some of those less-than-safe places are also ideal for sight-seeing and discovery. After all, you might never get back to this region of the world again – why not take advantage of the opportunity?

Here’s the question to ask yourself: when a political or civil uprising occurs, will your company support your evacuation? If your business has concluded and you’re touring Egypt’s historic sites only to find yourself in a desperate situation and need a security evacuation, your company may arrange for that evacuation but they may not.

Some travel insurance plans cover security and political evacuations when the conditions where the traveler is become unsafe. Escaping these situations may depend on the traveler’s level of knowledge, his or her ability to communicate in the local language, and whether commercial transportation options are available, but a travel insurance representative can help a desperate traveler negotiate those situations.

If your business doesn’t cover these situations, and you’re a frequent business traveler it could be in your best interest to purchase your own coverage. See the best travel insurance plans for business travelers for more details.

7. If you’re taking the kids, can they get home alone?

One of the concerns  – especially for single parents traveling with their children – is how the children will be cared for and/or transported home if something happens to the parent. If you attend a conference with child care for your little ones and extend your business trip for a few days of fun with your kids but something happens and you’re hospitalized – who will take care of your kids?

Travel insurance plans with emergency medical reunion can bring a family member of friend to your bedside. Further, travel insurance plans with return of minor children coverage can coordinate the return of your children to their home so they are not left unattended.

A final word …

While extending business travel to include some pleasure travel is an ideal way for busy workers to maximize the benefits of their business travel, it also enters into a grey area when something happens on your trip and you need help. Ideally, business travelers will be covered by a business travel insurance plan purchased through the company, but it not, it’s worth it to many business travelers to have coverage of their own.

5 Steps to Safer Off-Grid Travel

In 2010, the New York Times ran a story about five neuroscientists who took a rafting trip in the Glen Canyon National Recreation Area in Utah. The intent of the trip was to understand how the heavy use of digital devices and electronic technology changes how we think and behave – and also how retreating from them can reverse the (often negative) effects.

In 2010, the New York Times ran a story about five neuroscientists who took a rafting trip in the Glen Canyon National Recreation Area in Utah. The intent of the trip was to understand how the heavy use of digital devices and electronic technology changes how we think and behave – and also how retreating from them can reverse the (often negative) effects.

This is is why everyone calls it a vacation – it’s a restorative break from our normal lives.

These days, there are many people interested in off-the-grid living for a wide range of reasons, both political and personal, and the travel industry has caught on. Once isolated to those willing to pitch a tent and fish for their dinner, off-grid travel has become increasingly popular with jungle retreats, luxury resorts, and even trailers that are dropped off at remote locations – just for you to enjoy.

How far you take your off-the-grid travel adventure can range from simply turning off your electronic devices and leaving the car parked in favor of riding bikes all the way to sleeping in a hammock on a sustainable farm, eating only what you help produce, and showering in collected water.

If the idea of being in some remote area and fending for yourself appeals to you, there is still the question of safety. The following are five steps to prepare to stay safe when you travel off the grid.

1. Know your limits

Even if the chaos of your daily life has driven you to want a digital break, it’s important to know your limits. If you cannot live without your news fix, but you can take a break from reading hundreds of emails and tweeting what you had for lunch, factor that in. Leave your laptop or tablet at home, get your news fix at breakfast from a good old-fashioned television station and you’ve made a change you can live with on vacation.

We found some recommendations for how to digitally detox weeks ahead of your vacation to ensure that you really can go (and stay) off the grid for that amount of time (apparently this is incredibly tough for some folks).

2. Pack the essentials

Loads of off grid travelers take themselves to very remote places – often far out of range of good medical care. Sure, you’ll probably spend most of your day hiking, swimming, or even working the fields if you’re contributing to a sustainable farm as your payment for a bed to sleep in, but it still makes sense to wear sunscreen, stay well hydrated with clean, safe drinking water, and eat well.

Perhaps you don’t mind suffering through a headache, but if you cut your finger some antibacterial and a bandage wouldn’t be a bad idea. Take a little time to think about where you’re going, pack a travel medical kit, and don’t let an insect bite ruin your health on this trip.

3. Get the necessary vaccinations

Many off-grid travel locations are in unlikely and remote places. Some of those places can expose a traveler to unwanted and unwelcome diseases that they’re not likely to get back home. Many diseases common in other countries have been virtually eliminated in the U.S. Depending on your vaccination records, you may need a booster or a vaccination you never needed prior.

Do a little research about your destination so you know what items to bring and what vaccinations to get ahead of time. See our traveler’s vaccination checklist for more details.

4. Have an emergency plan

This is the one most travelers – even those not going off grid – forget and it’s unfortunate because some pre-trip planning can make all the difference. Anytime you’re traveling, it’s a good idea to let someone know where you’ll be and when you’re expected back. After all, if you don’t show up, help can be sent.

-

Keep your travel cash and a backup credit card secure in a money belt.

-

Know how to find medical help at your destination.

-

Store your travel documents securely and leave a backup with someone you trust.

-

Have some basic understanding of local laws so you avoid being arrested.

If you’re leaving behind all electronics, find out if where you’re going has a landline, a radio, or some way to get in touch in an emergency. Hint: even a whitewater rafting guide has to check in sometimes. If they don’t, consider the option of taking along a charged cell phone and turn it off unless you have an emergency.

5. Have travel insurance

Travel insurance is even more important when you’re traveling to a remote location where there are few medical facilities. If you are badly injured or become severely ill, you’ll need a travel insurance plan with coverage to take you to safety. Ensure that your travel insurance plan will cover your emergency medical treatment costs as well as your medical evacuation costs before you take your off-grid trip.

A final word about off-grid travel …

Some travelers find it very easy to get into the new no-digital routine, but while you’re traveling off the grid, it’s important to remember some basic safety rules too:

-

Let someone know when you’re going hiking, swimming, etc. Even better, take a buddy along with you.

-

Don’t touch the weird looking things. In remote places, you’re likely to encounter plants, insects, fruits, and more that you’ve never seen before. Unless you know what it is, don’t touch it.

-

Respect the neighbors you do have. Some remote eco-resorts, for instance, are also populated with wild animals, snakes, rodents and more. The best way to stay safe is to respect their space.

See also our 7 Essential Travel Products for Of-the-Grid Trips for a few more ideas when you’re planning your next trip.