Top Picks

for Trip Insurance

Expert picks from a licensed agent so you can find the the best plans fast.

Start my quote

You want to understand it,

before you buy it

Browse guides and 100’s of expert articles covering everything you need to know about travel insurance.

Get no-nonsense advice on:

- Why you should purchase travel insurance

- What travel insurance covers

- How much travel insurance costs

Expert picks for the best travel insurance plans. I dig in to find the coverage details that matter and explain it simply.

Check out our list of Best Travel Insurance policies.

- Best Overall

- Best for Covid-19

- Best for Cruises

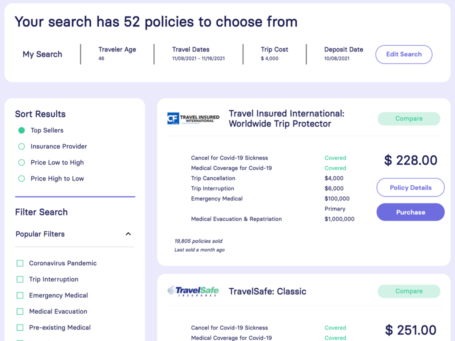

Get quotes from all major companies and save time. Compare plans to find the best coverage.

Just enter a few trip details and get instant quotes

- Instant quotes from all companies

- Easily compare plans to find the best coverage and price

- Guaranteed lowest price regulated by law

Protect your trip

Get the right coverage to keep you, your family, and your belongings safe. Our policies cover you from a wide range of travel mishaps. Pick the plan that’s right for you.

- Trip Cancellation

- Medical Emergencies

- Emergency Evacuation

- Lost & Stolen baggage

- Flight Delays and More

Trustworthy and reputable insurance providers

We only work with trustworthy companies. The Zero Complaint Guarantee is a promise that the travel insurance policy you purchase through our partner is from a reputable provider who will handle your claim fairly and honestly.

- Licensed claims adjusters to mediate on your behalf

- Insurance rates are regulated by law

- You can’t find the same insurance plans for a lower price anywhere else

Get instant quotes from all

major providers in minutes

-

Tell us about your trip

Answer a few simple questions about your destination, travel dates, travelers, and trip cost

-

Get instant quotes

We help you compare coverage, cost, and identify the best policies by focusing on your priorities and making it easy to understand

-

Purchase in minutes

Fast and easy checkout with immediate email confirmation of coverage

Learn travel insurance from the experts

Travel insurance for…

Covid-19 (Coronavirus)

-

Coronavirus "Cancel For Any Reason (CFAR)" Travel Insurance

This page is about travel insurance with Cancel For Any Reason coverage for coronavirus. For information about "travel medical only" insurance with coronavirus, go here. What is 'Cancel for any Reason' Coverage Cancel for any reason coverage is a type of trip cancellation coverage. It's also one of the primary reasons travelers purchase travel insurance. Here's the important part: standard trip cancellation coverage doesn't include canceling for an outbreak of a pandemic like COVID. With Cancel for any reason coverage, or CFAR, travelers can cancel their trips for any reason, including COVID. The coverage reimburses you up to 75% of your initial trip costs if you have to cancel a trip. See Cancel for any Reason (CFAR) Travel Insurance Coverage for a full explanation. CFAR Travel Insurance for COVID-19 Travel insurance with Cancel For Any Reason (CFAR) coverage has become very popular since the coronavirus (COVID-19) outbreak earlier this year.…

-

Travel Medical Insurance for Coronavirus

This page is about travel medical insurance for coronavirus, which does not cover canceled trips. For information about trip cancellation insurance and coronavirus, go here. Who this page is for Travelers who are planning a trip outside their home country, and want insurance to pay expenses in case they get coronavirus. Overview of Travel Medical Insurance Travel medical insurance is something you should purchase whenever you leave your home country. It covers emergency medical expenses from accidents and illnesses, evacuation costs, and acts as a lifeline to call in a foreign country. Because, when you leave your home country, your health insurance from home might not travel with you. Medicare never covers you abroad. Even if your insurer from home does cover medical costs, there is likely a costly deductible. Plus, even if your insurance from home covers medical expenses, they won't cover evacuation costs which could be financially ruining…

-

What if you get COVID while traveling?

We’ve all gotten used to an endless array of hygienic measures, mask mandates, pre-travel testing, and vaccinations to reduce the risk of contracting or spreading COVID-19. The new and rapidly spreading variant has caused a new round of global uncertainty and travel restrictions. In the latest shakeup of travel news, two countries (England and Israel) have ditched the pre-arrival tests for incoming travelers. As the world continues to navigate the COVID-19 pandemic and works to decide what endemic means, the question-of-the-week on travelers’ minds is what to do if they get COVID while traveling. If you’re ready to travel and concerned about testing positive or getting sick with COVID-19 while away from home, here are the answers to your top questions. Q: What can I do to be prepared? Expecting the unexpected is part of travel planning and it’s even more essential now. Here are five critical steps to complete to be prepared…

Travel insurance for…

Traveling with families

-

11 Reasons to Buy Travel Insurance

We know travel insurance can seem like just one more expense, and many travelers ask the question why buy travel insurance and why get travel insurance? Here are the most important reasons to buy travel insurance. 1. You need to cancel your trip What happens if someone gets sick and can’t travel, a parent dies, you’re required to work, or your house floods? With trip cancellation coverage, you’ll be able to recover your out-of-pocket expenses for these covered reasons and more. 2. You miss your connection You’ve planned a cruise but you discover the connecting flight to get to the ship is delayed. With the missed connection it looks like you will miss your cruise departure. How will you catch up to the ship? With missed connection coverage, you can take another flight to catch the ship at the next port-of-call. You’ll also have assistance services to help you arrange and pay for those travel changes. 3. Your flight…

-

How Travel Insurance Covers Kids

The odds that something will happen to complicate or derail your travel plans with the kids has become the norm rather than the exception. Many travel insurance providers offer free travel insurance to cover kids who are traveling with their parents, guardians, even grandparents. Here's how travel insurance covers kids. Travel insurance plans include coverage for kids with these helpful benefits: Return of minors - this benefit ensures that minors will be cared for and returned home if the adult they are traveling with is hospitalized for a certain number of daysEmergency medical reunion - this benefit ensures that you won’t have to pay for airfare and accommodation to visit your kid if they are hospitalized away from youEvacuation - an evacuation to escape an oncoming hurricane for 2 is expensive enough, but add in a few kids and it can get downright cost-prohibitive. This benefit covers security evacuations when…

-

Cancel For Any Reason (CFAR) Travel Insurance Coverage

What is CFAR Travel Insurance? Briefly: Cancel For Any Reason (CFAR) is travel insurance coverage that reimburses up to 75% of your total trip costs if you have to cancel your trip for any reason not listed in the standard coverage. What you will find on this page: Coronavirus: Special Section & TipsHow does CFAR coverage help?What does Cancel For Any Reason travel insurance cover?How does CFAR work?Understanding Supplier Cancellation PenaltiesImportant notes about Cancel For Any Reason travel insuranceWhat type of policy covers this?How to buy a plan with Cancel For Any Reason coverageFAQs about Cancel For Any Reason insuranceCompany CFAR Coverage TableSummary Coronavirus: Special Section & Tips With the continued concerns about the Coronavirus outbreak, millions of travelers are not sure what to do about travel plans. Travel insurance can help in several ways, but it depends on the traveler, the trip, timing, and what is needed. Note: If you…

Travelers love CoverTrip. Have

a look for yourself

Daniel W.

“Honestly this website made it extremely easy. I don’t know what I would have done without it since I had no idea what I was doing. Really nice interface and tools. Much better than the googling I was doing before finding this website.”

Nancy L.

“I went to Google and found your site. It allowed me to get what I needed at a price that was friendly to my budget. Not only that, I was able to compare a few options to make sure I was getting exactly the coverage I needed. I will definitely recommend your site if the situation comes up among my friends.”

Ran P.

“The website was amazing in helping me understand better what I am buying and quickly comparing the best options. Thank you for your help.”

Amelia E.

“Finding travel insurance is frustrating but your articles and reviews made it easy to understand. Will definitely recommend your website!”

Michael M.

“Thanks! The info on your website was very helpful!”

Jennifer L.

“Our family is planning a Disney trip this Spring and your website made it very easy to find insurance. Hopefully we don’t need to use it!!”

Karin O.

“I was helping my parents plan a trip to Germany because I was nervous about medical insurance. I didn’t know anything about this coverage but your articles helped so much.”

Kathy T.

“Peace-of-mind knowing my family was covered for the “unexpected” during our trip to BVI. I will use your website again when we take our next trip”

Experienced

& trusted

Since 2006, over 11 million visitors have learned about travel insurance, read company reviews, and found the best plan for their trip with us

Travel Insurance Blog

We invented the game when it comes to travel insurance information

Trips covered with us

We help travelers find the best insurance. Period.